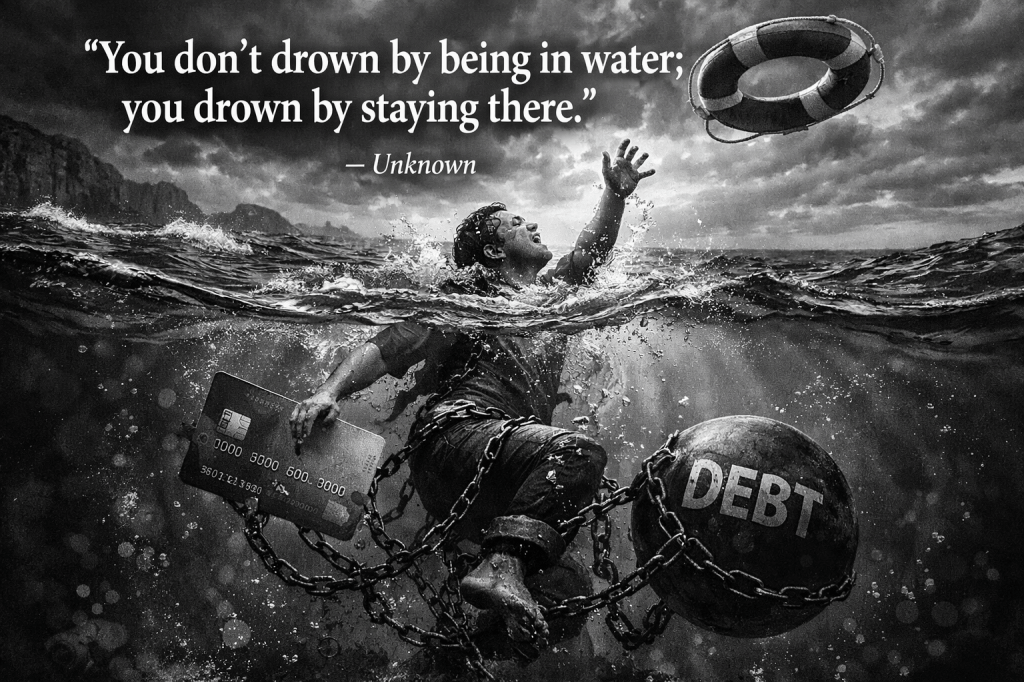

“You don’t drown by being in water; you drown by staying there.” – unknown

Debt is a complex, intimidating, and often confusing aspect of consumer finance. Whether it is a personal loan, credit card debt, or other forms of consumer lending, most adults have to face it at some point during their life.

Here are three simple notes of caution for consumer debt that can prove useful if you find yourself in a situation evaluating options:

Do Not Swim With Sharks

Predatory lenders are often referred to as “loan sharks.”

A great explanation from the dictionary:

Loan Shark: a moneylender who charges extremely high rates of interest, typically under illegal conditions.

Reports of exploitation and deceptive trading practices by loan sharks.

Definitions from Oxford Languages

While not considered loan sharks due to still being highly regulated, many merchandise credit cards offer minimal benefits while charging astronomical interest. I have even seen personal loans with 300% interest!

This is not simply unethical, it is financially dangerous.

Do Not Go Swimming During a Storm

Merchandise or consumer commercial lending offers typically target people in vulnerable positions. Here are a few examples:

You need some repairs done on your car, but you don’t have the cash. The auto shop may have a third-party lender who will finance your repair…at a 40% APR.

You have a large bill that you did not expect and need to find a way to cover it. You do some online research and find a personal $3,000 loan. You think you’ve found the solution, until you learn that it is a 3 month lending period with a 60% interest rate.

Situations like these, and many others, are often the reason people don’t simply get into debt, but stay there.

Check the Weather Forecast

While many bank or credit union credit cards offer tremendous benefits, it is important to ask yourself some realistic questions before ever pursuing debt as a financing strategy:

- Do you have the discipline to spend within your income, not your credit limit?

- Are the benefits worth the risk of carrying a balance on the card? Look at the costs vs. the rewards.

- Do you use the benefits or points frequently enough for the offer to be beneficial to you personally, not just a good credit card program? You don’t need a credit card that earns you flyer miles if you never travel.

An important distinction to know before engaging with debt: APR and Interest Rates are NOT the same. They are NOT equivalent or interchangeable terms.

APR: The cost to borrow the principal plus fees, providing a more accurate reflection of the total cost.

Interest Rate: The cost to borrow the principal amount.

Why does this distinction matter? Because not every credit card charges fees, or at least, the same amount of fees. Not every loan has an outlandish interest rate, but heavy and extensive fee structures.

The APR is a more accurate perspective on what it will cost you to stay in the water.

The Interest Rate is a good tool to use when evaluating your need for increased cash flow.

Not all debt is bad. Not every lender or credit card program is designed by sharks. But if you get into the water, do not stay there. Or you will drown.

Do not get into loan shark infested waters.

You don’t drown by being in water; you drown by staying there.

3.5.2026

By Noah Cisneros

Disclaimer:

This article is not sponsored or approved by any financial institution that I am associated with. I am NOT a certified personal financial advisor. I am NOT a professional investor. This article is purely educational to provide helpful ideas to improve life. Please use the tools within your reach to personally make any and all decisions for your finances.